{kind=link}

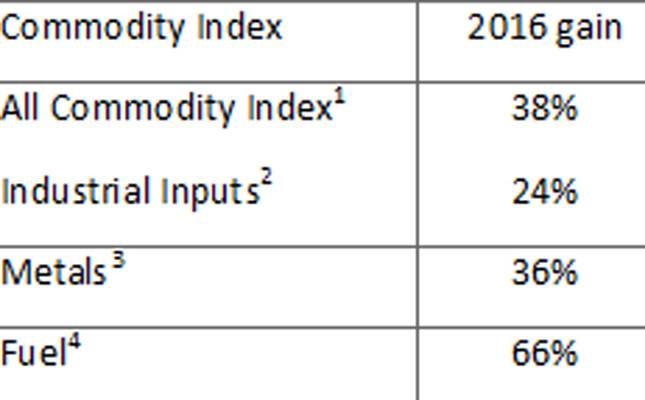

However, the scale of revival in prices since then has been almost unprecedented in the post-financial crisis era.

{kind=link}

Data source : IMF

1. All Commodity Price Index includes both Fuel and Non-Fuel Price Indices

2. Industrial Inputs Price Index includes Agricultural Raw Materials and Metals Price Indices

3. Metals Price Index includes Copper, Aluminium, Iron Ore, Tin, Nickel, Zinc, Lead, and Uranium Price Indices

4. Fuel (Energy) Index includes Crude oil (petroleum), Natural Gas, and Coal Price Indices

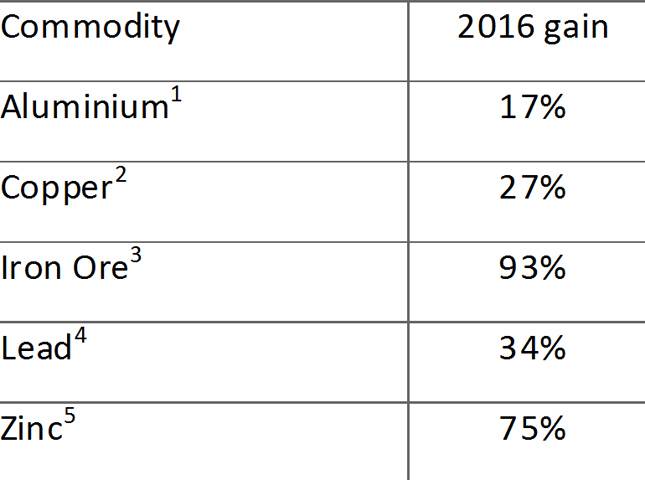

While Energy prices stand out with their 66% gain over the course of 2016, the rally in Metals prices took many by surprise. All the commonly used metals have rallied sharply on the back of expectations of a large infrastructure push in the US under the Trump Presidency and Chinese demand:

1. Aluminium, 99.5% minimum purity, LME spot price

2. Copper, grade A cathode, LME spot price

3. China import Iron Ore Fines 62% FE spot

4. Lead, 99.97% pure, LME spot price

5. Zinc, high grade 98% pure

{kind=link}

The above gains are in US Dollar terms. During 2016, the Indian Rupee has depreciated by nearly 4% from around Rs 65.9/USD at the beginning of the year to above Rs 68.3/USD at the end, which has exacerbated the cost escalation for Indian buyers.

Liquid gold

Of all the industrial commodities, oil is perhaps the most relevant for industry given that many inputs are crude oil derivatives. Prominent industries like Paints, Rubber, Plastics, and Petrochemicals are subject to the vagaries of oil markets – the correlation between oil prices and the petrochemical inputs required for these sectors is approximately 0.65-0.75 as per analyst estimates.

Brent crude had fallen to a 12-year low of $27.88 per barrel on 20 January 2016. Since then, it recovered to about $55 plus per barrel towards the end of the year – a doubling of prices within a year!

Most analysts believe that Indian industry will start hurting at current levels and that if oil prices cross $70 per barrel, it will spell major trouble. Despite rising prices, India’s fuel consumption surged 10.9% to 183.5 million tonnes in FY16 as per Oil Ministry data. The Ministry forecasts a 9% growth to 200 million tonnes for FY17.

The run up in prices was not entirely surprising though, as per some commodity traders like Akshay Malhotra, Chemicals Trader at Tricon International. “The collapse in oil prices towards the end of 2014, when crude fell from $110 to $50 levels, as well as the fall towards the end of 2015, when prices went from $60+ to as low as $28, took many by surprise. This led to a major reworking of predictions and models. Considering this, the rally in 2016 was in line with market expectations if you compare the performance in the last 3 years,” he opines.

While the impact of such sizeable rises in input prices has been felt across the board, SMEs, in particular are badly impacted by the rising input prices due to the following factors:

Scale: SMEs have lower negotiating power due to the relatively smaller size of their purchases.

Insufficient hedging: Smaller businesses have lower awareness of and lesser access to hedging options covering both commodity prices and currency movements.

Cash dependence: The demonetisation move came when prices were peaking. This resulted in a dual hit – the limited cash and high prices meant that volumes had to be curtailed. The demand scenario is also in a situation where higher costs cannot be easily passed on.

There are also many second order effects on smaller businesses. Malhotra adds, “Demonetisation has impacted the local distributors of petrochemicals as most of them sell to smaller players who either deal in cash or PDCs. The demand has not reduced substantially, but the financial impact is greater with distributors reworking their credit arrangements and financing options with banks due to the ripple effect of delayed cash recovery/revenue collection from their smaller customers. Another effect being seen is that higher commodity prices coupled with lower demand leads players to look for cheaper alternates and substitutes in the market.”

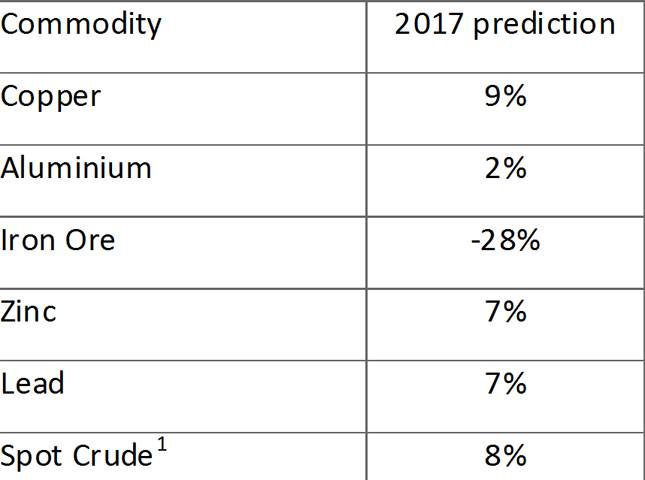

Outlook

After the 2016 mega-rally, most analysts are predicting further gains in 2017 for most commodities, though modest in range compared to the past year. As per IMF predictions, iron ore is, in fact up for a large correction after the near doubling of prices in 2016.

Average of spot prices for UK Brent, Dubai and West Texas Intermediate

{kind=link}

There is also great diffidence among oil analysts. There are lingering doubts over the actual extent of OPEC cuts, which have fed the rally in the last couple of months. As per IMF, “The actual impact of the [OPEC cut] agreement will depend on the degree of compliance by OPEC countries, non-OPEC oil producers’ cooperation, and shale responses. In the past, OPEC members tended to produce more than their quota to meet their finance needs. Most importantly, shale production might rebound strongly.”

Sentiment has also worsened by concerns over the health of the Chinese economy after it reported the steepest falls in exports since 2009. If these concerns prove correct then there could be some relief in store for oil consuming sectors.

Be that as it may, SMEs can ill afford further volatility or rising prices in a demand-stressed scenario. Hedging mechanisms that provide a cushion against rising prices are gaining popularity in India and some of these will be covered in Part 2 of this article.

Source: The Economic Times